What You Should Know

Florida has more sinkholes than any other state in the nation. However, not all homeowners’ policies provide coverage for damage to your home resulting from sinkholes. Florida law only requires insurance companies to cover

“catastrophic ground cover collapse.”

All insurance companies licensed in Florida must “offer” sinkhole coverage, however, it usually is an endorsement to an existing policy and costs additional premium. Insurance companies may require an inspection before extending sinkhole coverage. If sinkhole activity is present on the property or within a certain distance of the property to be insured, the insurance company may decline to provide sinkhole coverage.

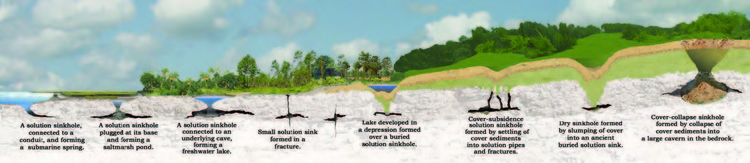

Florida law defines “sinkhole” as “a land

form created by subsidence of soil, sediment or rock as underlying strata are dissolved by groundwater. A sinkhole may form by collapse into subterranean voids created by dissolution (the dissolving) of limestone or dolostone or by the subsidence as these strata are dissolved.”

“Catastrophic ground cover collapse” is defined as “geological activity that results in all of the following:

1. The abrupt collapse of the ground cover;

2. A depression in the ground cover clearly visible to the naked eye;

3. Structural damage to the building including the foundation; and

4. The insured structure being condemned and ordered

to be vacated by the government agency authorized by law to issue such an order for that structure.”

f you do not purchase sinkhole coverage and your home is damaged by sinkhole activity,

the only coverage you have is for catastrophic ground cover collapse and if the damage does not meet all four criteria required for catastrophic ground cover collapse – for instance, you may have foundation cracks, but the home is still livable – your insurance company may not pay for the damage.

If You Are Buying a Home

• Call an insurance agent to determine whether the home is insurable.

• Check with your city or county officials about recent sinkhole activity in the area.

• If you want to purchase sinkhole coverage, be sure to tell your insurance agent and make sure the coverage is included in your policy or a rider.

• Hire a home inspector who can help you identify signs of potential sinkhole activity, like cracks in the foundation or walls.

• Consider sinkhole testing. While infrequent, an insurance company may require you to have this testing done prior to granting you coverage, under certain circumstances. 4-point inspections normally required by your lender do not address the potential for sinkholes on your property.

If You Have a Sinkhole Claim

Here are some immediate steps you should take if a sinkhole has opened on your property, or if a portion of your home has shifted or sunk due to ground cover collapse:

Here are some immediate steps you should take if a sinkhole has opened on your property, or if a portion of your home has shifted or sunk due to ground cover collapse:

• Provide for the personal safety of your family. Evacuate, if necessary.

• Secure or remove your valuable possessions, if you can do so safely.

• Notify your insurance company or insurance agent immediately.

• Notify your city or county building inspection department.

• Mark the sinkhole or property

with fencing, rope or tape to warn others of the danger. You could be held liable if someone is injured on your property.

• If you have sinkhole coverage, your insurance company will probably perform geological testing that will establish the cause of the damage. If the testing confirms that a sinkhole was the cause, your insurance policy should pay for the testing and repairs, less any applicable deductibles.